Buying a house will usually require you to put down a deposit of 10% — 20% of the purchase price upfront.

However, there is the option of acquiring a 100% home loan, which will remove the need to pay a deposit as the loan is funded entirely through monthly repayments.

You can determine what home loan you’re likely to qualify for, and what your monthly repayments will be, using our Bond Calculator. This will help you plan your budget, factoring in the cost of the deposit.

Being pre-approved doesn’t mean you’re approved. It means you have an idea of what you would likely qualify for.

The pre-approval process takes into account your credit score and determines the size of the home loan you would qualify for.

It does, however, provide proof you can afford the amount for which you’ve prequalified. This proof can be useful when dealing with the property seller.

It also helps with your house hunt, as you know the price bracket you should be looking at if you want to improve your chance of home loan approval.

You can get pre-approved by contacting Green Eye Housing or by using our free, online prequalification tool, the Bond Indicator.

If you are unable to pay off debts, your name will be flagged by the credit bureau, and added to a blacklist; and it will be more difficult for you to get loans in the future.

The simplest way to clear your name from the credit bureau is to pay off the debt. According to TransUnion, one of South Africa’ biggest credit bureaus, this will usually result in your name being removed from the blacklist within 7 – 20 days.

You can also request that your creditor write to the credit bureau to notify them that the debt has been paid, and that they can remove your name from the list, although your creditor is not obligated to do this.

If you are struggling to pay off debts, you should consider going into debt counselling.

If you are concerned about the prospect of being blacklisted, you can check your credit record to see what your standing is. We can provide you with your credit score if you apply for home loan prequalification, either by using our free, online tool, the Bond Indicator, or by contacting us at Green Eye Housing.

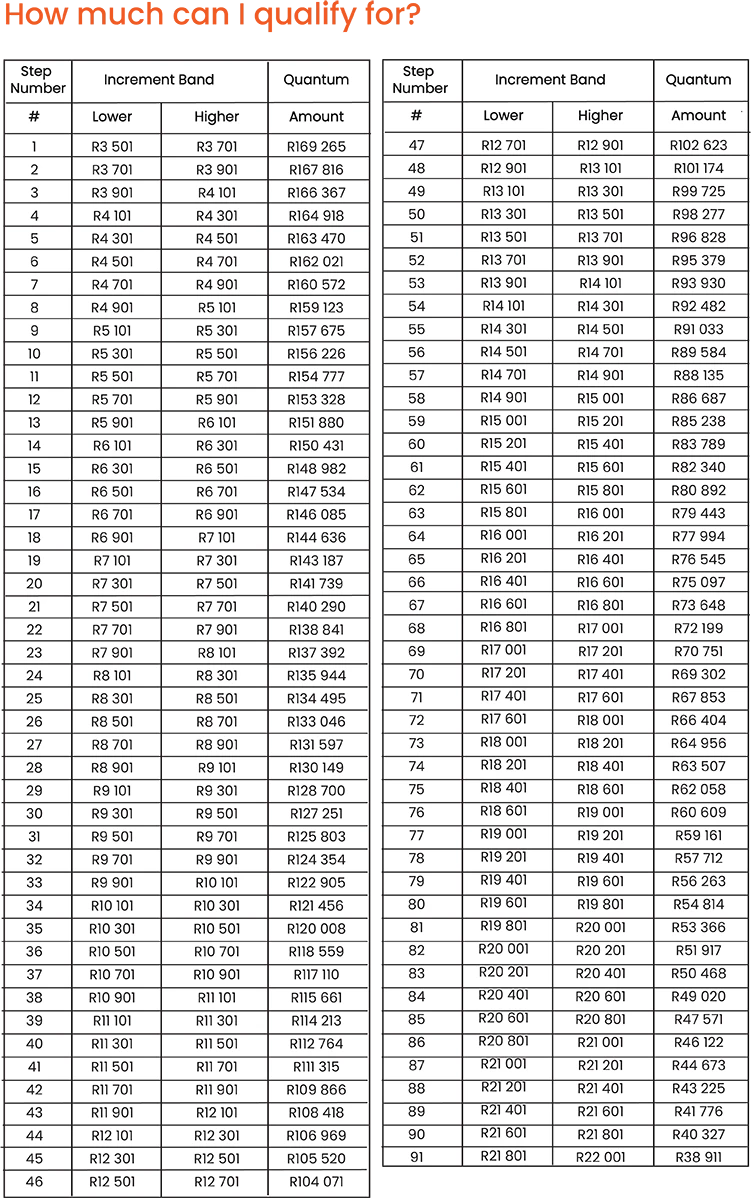

To qualify for FLISP, you must have an income of R3501—R22 000 per month. Then, the lower your income within that bracket, the higher your subsidy.

For low and middle-income earners, FLISP provides a government subsidy for your home loan. The size of the subsidy depends on your income.

Your income must be in the R3 501 to R22 000 per month bracket to qualify for FLISP.

Then, the lower your income within that bracket, the higher your subsidy.

The subsidy ranges from R30 001 to R130 000.

For a more detailed look at subsidies, you may peruse the table below:

You can apply for a bond with anyone you choose: a partner, (even if you’re not married), a friend, or with one or multiple family members. Just make sure you have a legal agreement drawn up between the parties in question to protect all of your interests.

What do the banks look at when considering my home loan application?

The first thing the banks will do is review your credit score. Then they will look at your income and expenses to gauge your ability to repay the monthly home loan instalments. They will also take the size of your deposit (if you have one) into account.